I am pleased to share with readers our Oct. 27, 2020 post to subscribers of GlobalSource Partners (globalsourcepartners.com), a New York-based network of independent emerging markets analysts. Christine Tang and I are their Philippine Advisors.

Amidst a succession of GDP growth downgrades, most recently by the IMF, we are watching three developments this month that signal better prospects heading into 2021.

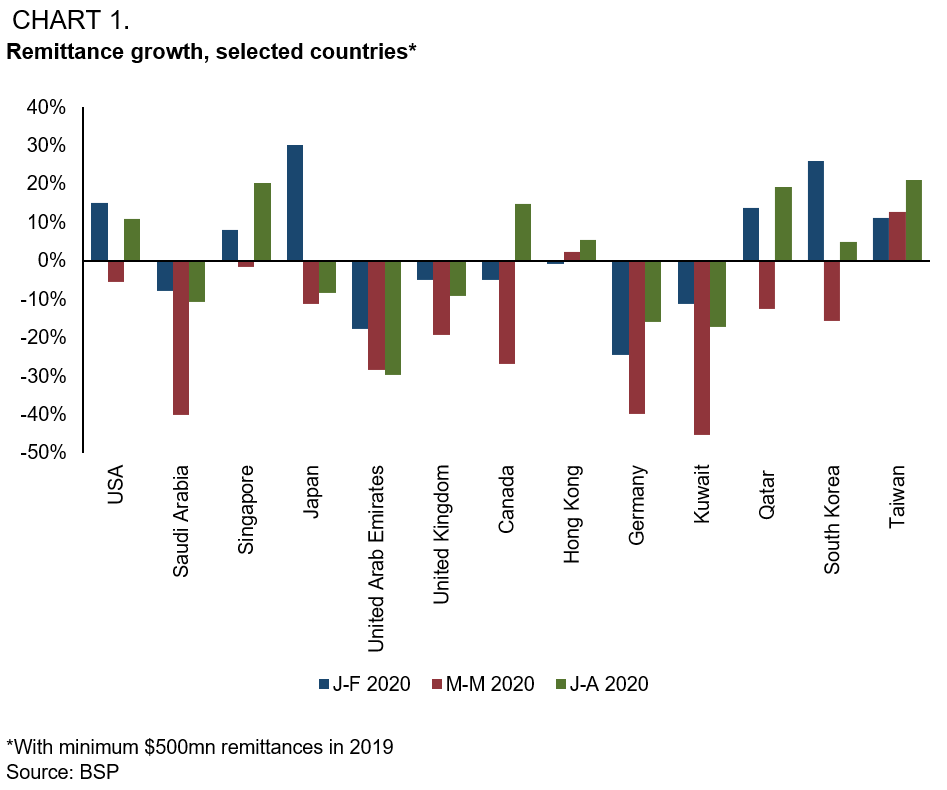

1. Remittances have surprised on the upside. Monies sent home have expectedly declined but not as much as anticipated. After plummeting by double digits in April and May year on year, the inflows rebounded in June and July, each by nearly 8%, then slipped again in August but only by 4%. For the six-month period since the pandemic started (from March to August), remittances fell moderately by 5% year on year, bringing the year to August decline to only 2.6%. This is good news considering that in our last outlook report, we were expecting a 7% contraction for the year. (The ADB and the World Bank forecast double digit drops in remittance inflows earlier in the year.)

What appears to be driving the stronger than expected remittances are inflows from countries that have large Filipino migrant populations (US and Canada) where the respective governments have also provided generous fiscal support, including wage subsidies (e.g., US, Singapore), and/or have managed the outbreak relatively better (e.g., east Asian economies). Too, despite the bust in cruise tourism, remittances from seafarers have also performed better that expected due to improved trade volumes in 3Q.

Nevertheless, there are still significant downside risks moving forward with several host countries facing a resurgence of COVID-19 (including the US and in Europe) that risks keeping unemployment high for longer, and the prospect of continuing low oil prices weighing down oil exporting economies, particularly in the Middle East which host many overseas Filipino workers.

At the same time, remittances may come under renewed pressure as fiscal packages are downsized or withdrawn following sharp increases in public debts, more businesses closing shop especially in the service sector where many overseas Filipino workers, and possible waning of momentum in global trade amidst continuing geopolitical uncertainties. Moreover, despite better than expected dollar remittances, the peso’s over 4% appreciation so far this year reduces the support to domestic consumption.

2. After a dramatic speakership fight at the House of Representatives early this month that provoked a televised presidential rebuke and necessitated the calling of a special session of Congress to pass the 2021 national budget, the Lower House under a new leadership quickly approved the spending bill that is expected to be sent to the Senate today. Considering the President’s certification of the bill as urgent for the government’s continuing struggle against COVID-19, expectations are that a new appropriations law will be ready by the start of next year.

Yet, while the P4.5-trillion (22% of GDP) budget, which is 10% above this year’s approved budget (excluding supplemental funds under the Bayanihan Act), appears on paper to be responsive to the COVID-19 crisis (with proposed spending priorities for health, infrastructure development, and post-pandemic adaptation), a lingering question is how well the executive can implement the plans and programs. Reports indicate failures at the height of the pandemic to distribute allocated social amelioration funds both fully and in a timely way. Also, out of the P140-billion supplemental budget approved in September, the budget department reported that releases have only totaled P4.4 billion with P46.2 billion pending approval of the Office of the President and the remaining P89.4 billion still awaiting requests from the concerned departments. Given fiscal authorities’ relatively conservative stance in the fight against COVID-19, underspending a limited budget would be tragic especially in the face of the pandemic’s disproportionate impact on lower income groups.

3. Now into the eighth month of varying lockdown stringency, the Philippine government is finally attempting in earnest to open the economy. After flip-flopping last month, it has proceeded to reduce distancing protocols for public transport to maximize the share of the economy allowed to open under the latest guidelines (about 65% per the planning secretary vs. only 50% effectively if those who are allowed to work have no means of getting to work). It has also allowed more age groups to leave homes, reduced curfew hours, and eased tourism restrictions including allowing outbound travel and local hotels to operate at 100% capacity. The decision resulted from a full cabinet meeting early this month and was taken subject to the conditions that everyone observes the minimum health standards and that hospital capacity remains below the 70% threshold (the latest occupancy rate is 52% in Metro Manila).The move to open up the economy is being done at a time when there appears to be some plateauing of the COVID-19 infection curve, with the doubling time lengthening since late August and the reproduction number falling below 1. The caveat however is that since Oct 16, testing has dropped significantly as the Philippine Red Cross (PRC) stopped accepting the state insurance agency’s credit for non-payment of about P1 billion in arrears. Prior to the suspension, the PRC was conducting about a third of the 30,000 tests done on average per day. Too, challenges remain in isolating individuals who have tested positive for the coronavirus as well as in contact tracing, critical functions for successfully suppressing the virus per the experience of other countries. Hence, while it is good news that the government has finally taken the tough decision to “dance” with COVID-19, diligently planning the steps for opening the economy while managing health risks, many harbor lingering concerns about implementation, the Philippine’s Achilles heel.